If you’ve had a car written off by an insurer, or you’re considering buying a car with write-off history, understanding the category system is essential. The categories determine whether a car can be legally returned to the road, and they have significant implications for value, insurability, and safety. Here’s a plain-English explanation of what each category means.

Why Cars Get Written Off

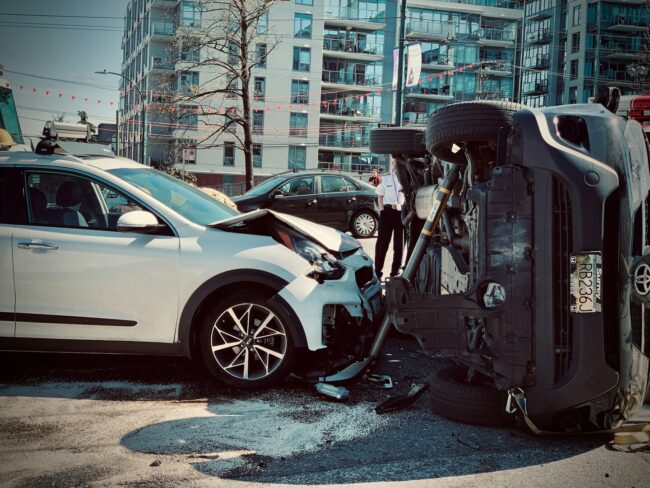

A car is declared a write-off (technically a “total loss”) by an insurer when the cost of repairing it exceeds a threshold relative to its market value — typically when repair costs would exceed around 50–60% of the car’s pre-accident value, though this varies by insurer. It doesn’t necessarily mean the car is destroyed or even severely damaged. A relatively minor impact on an expensive, low-mileage car can result in a write-off if the repair bill is disproportionate.

Category A: Scrap Only

Category A is the most severe classification. A Cat A vehicle must be crushed in its entirety — no parts may be salvaged, no components may be reused. This category is reserved for vehicles so severely damaged that nothing is safe to reuse. Cat A vehicles should never appear for sale. If you encounter one, it’s either a scam or a serious legal and safety issue.

Category B: Body Shell Must Be Crushed

Category B vehicles must have their body shell crushed, but working mechanical and electrical components can be salvaged and sold for use in other vehicles. The car itself cannot be repaired and returned to the road in any form. Like Cat A, Cat B vehicles should never appear for sale as driveable cars. If a car appears on a history check as Category B, walk away.

Category S: Structural Damage, Repaired

Category S (previously Category C) means the car suffered structural damage — damage to the chassis, monocoque body shell, or other load-bearing components — but has been (or can be) professionally repaired and returned to the road. A Cat S write-off can be legally sold and driven, but the write-off status must be disclosed and the car must be re-registered with the DVLA before it returns to the road.

The key question with a Cat S vehicle is the quality of the structural repair. Structural damage, if improperly repaired, can affect the car’s ability to protect occupants in a subsequent accident. A professional inspection by a specialist — using equipment to check structural geometry — is strongly advisable before buying any Cat S vehicle.

Cat S cars sell at a significant discount to equivalent undamaged examples — typically 20–40% less, depending on make, model, and quality of repair. For a buyer who does thorough due diligence, they can represent value. For a buyer who doesn’t, they can be a dangerous and expensive mistake.

Category N: Non-Structural Damage, Repaired

Category N (previously Category D) means the car suffered non-structural damage — cosmetic damage, electrical faults, or mechanical damage that doesn’t involve structural components. It can be repaired and returned to the road, and must be disclosed as a write-off.

The discount on Cat N vehicles is typically less than on Cat S — perhaps 10–25% — because the damage type is less severe. However, non-structural doesn’t mean trivial. Electrical damage in modern cars can be extensive and difficult to fully resolve, and some Cat N write-offs have persistent gremlins that affect reliability and value.

How to Check Write-Off Status

A vehicle history check — HPI, Experian, or similar — will reveal whether a car has been recorded as a write-off and, if so, which category. The DVLA also holds this information on the vehicle register. Always run a history check before buying any used car.

Note that not all write-offs are recorded immediately. Some insurers are slower to update the databases than others, and there’s a small risk that a recently written-off car won’t yet appear on a check. Buying from a reputable source and using a specialist inspection reduces but doesn’t entirely eliminate this risk.

Insuring a Write-Off Category Car

Cat S and Cat N cars can be insured, but not all insurers will cover them, and those that do may charge higher premiums. When obtaining a quote, you must disclose the write-off history. Failing to do so is material non-disclosure and can invalidate your policy.

Some specialist insurers are more comfortable with write-off history than standard market insurers. It’s worth using a broker rather than just a comparison site if you’re struggling to find reasonable cover.

The Old Category System

Prior to October 2017, the categories were A, B, C, and D. Categories C and D broadly correspond to the current S and N categories. If you see a car listed as Cat C or Cat D, it was written off before 2017 under the old system. The principles are the same — structural versus non-structural damage — but the labelling is different. Don’t confuse the old D category with Cat D on credit reference files (which is something else entirely).

Should You Buy a Write-Off Category Car?

Cat S with a professional inspection and a provably high-quality repair can represent genuine value — particularly on a desirable car where the price reduction is significant. Cat N is lower risk by definition, though electrical gremlins can be persistent. In both cases, the discount must be sufficient to justify the residual uncertainty and the impact on future resale value — because you’ll face the same disclosure obligation when you come to sell.

Leave a Reply